Issue #7: The GLP-1 Gold Rush

The fastest-growing drug class in history costs 3-5x more in America. We modeled what happens when Medicare starts paying.

Every issue of The American Healthcare Conundrum identifies one fixable, quantifiable problem in the US healthcare system, builds the data case, and recommends a specific policy fix. All code and data are open-source.

SAVINGS TRACKER

Target: ~$3T US-Japan per-capita gap

Japan: highest life expectancy, lowest

infant mortality in OECD, ~half US cost

Full scale: $0 ──────────────── $3T

████████░░░░░░░░░░ 13.2%

↑ $396.6B identified

Zoomed (first $500B):

#1 ░ $0.6B OTC Drug Overspending

#2 ███ +$25.0B Drug Pricing

#3 ██████████ +$73.0B Hospitals

#4 ████ +$30.0B PBM Reform

#5 ████████████████████████████ +$200.0B Admin Waste

#6 ████ +$28.0B Supply Waste

#7 █████ +$40.0B GLP-1 Pricing

─────────────────────────────────────────────

Total: $396.6B · $2,603.4B remaining

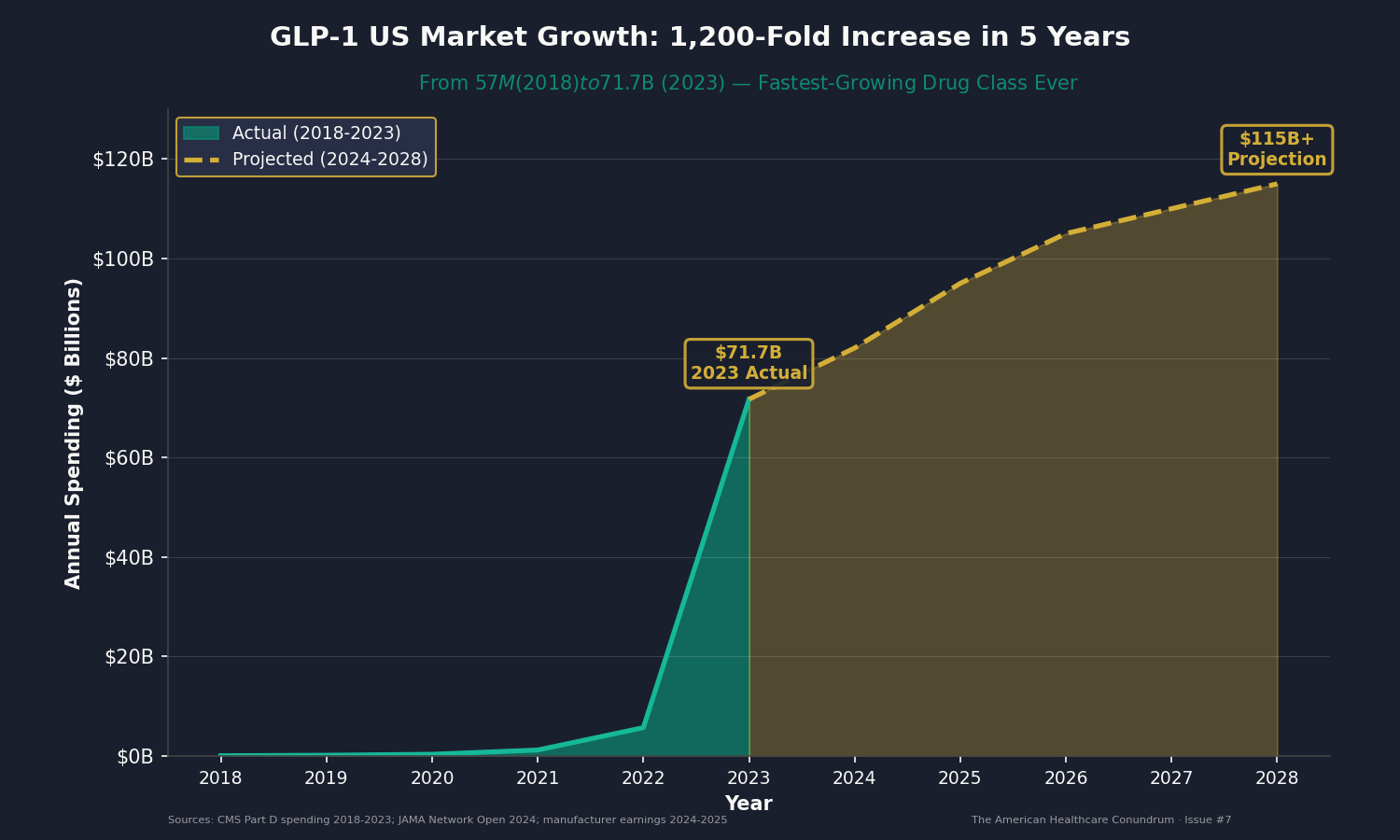

The GLP-1 Gold Rush

In 2018, the United States spent $57 million on GLP-1 receptor agonists. In 2023, it spent $71.7 billion. That is a 1,200-fold increase in five years, and the United States pays three to five times more per dose than every other country buying the same drug.

Novo Nordisk collected $26 billion from semaglutide products (Ozempic, Wegovy) in 2024. Eli Lilly is on track to exceed $35 billion from tirzepatide (Mounjaro, Zepbound) in 2025. Together, the two drugs now drive one-tenth of all US prescription spending growth.

In July 2026, Medicare launches the GLP-1 Bridge pilot, covering GLP-1 receptor agonists for obesity in beneficiaries, with the permanent BALANCE Model following in January 2027. This program is the first time a weight-loss drug has been paid for by public insurance at scale. We modeled the cost and identified something nobody else has yet published: the true 10-year budget impact of bringing millions of Medicare beneficiaries into negotiated-price GLP-1 coverage.

The Market: Fastest-Growing Drug Class Ever

Ozempic (semaglutide for type 2 diabetes) launched in the United States in 2017 at roughly $5 per pill. By 2022, it had become a blockbuster. Then Novo launched Wegovy, the same molecule under a different name for weight loss, in 2021. Eli Lilly launched Mounjaro (tirzepatide) for diabetes in 2022, then Zepbound (same drug) for obesity in 2023. The FDA approved the first oral versions in December 2025.

The scale is unprecedented. In 2018, total US GLP-1 spending was $57 million. Five years later, it was $71.7 billion. That is not a growth story. That is an emergence story: a drug class that did not exist in the healthcare market is now consuming 8.9% of all US prescription spending.

Manufacturers project the US market will exceed $100 billion by 2028. Some analysts predict $150 billion by 2030. This is what happens when you have a drug that works, that addresses a condition affecting 115 million American adults, and that costs more in the United States than anywhere else on Earth.

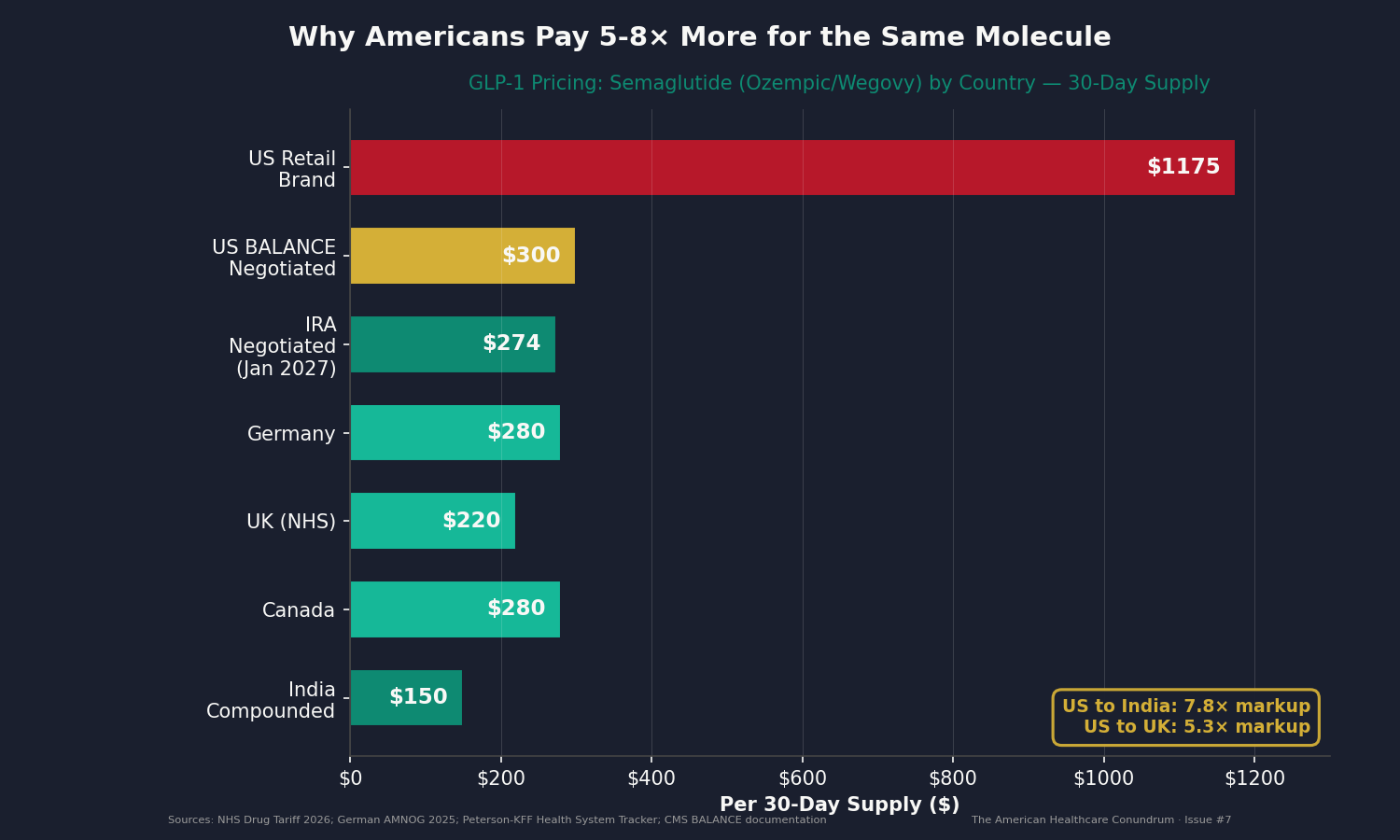

The Price Gap: Why $1,000 in America, $200 Abroad

A 30-day supply of semaglutide (Ozempic or Wegovy) costs approximately $1,000 to $1,350 per month in the United States without insurance. The same 30 days cost:

- $190 in the United Kingdom (NHS generic rate)

- $250 to $300 in Germany

- $250 to $300 in Canada

- $100 to $200 in India (compounded generic)

The US price for a single prescription represents a 5 to 13 times markup from India, and a 3 to 7 times markup from Europe.

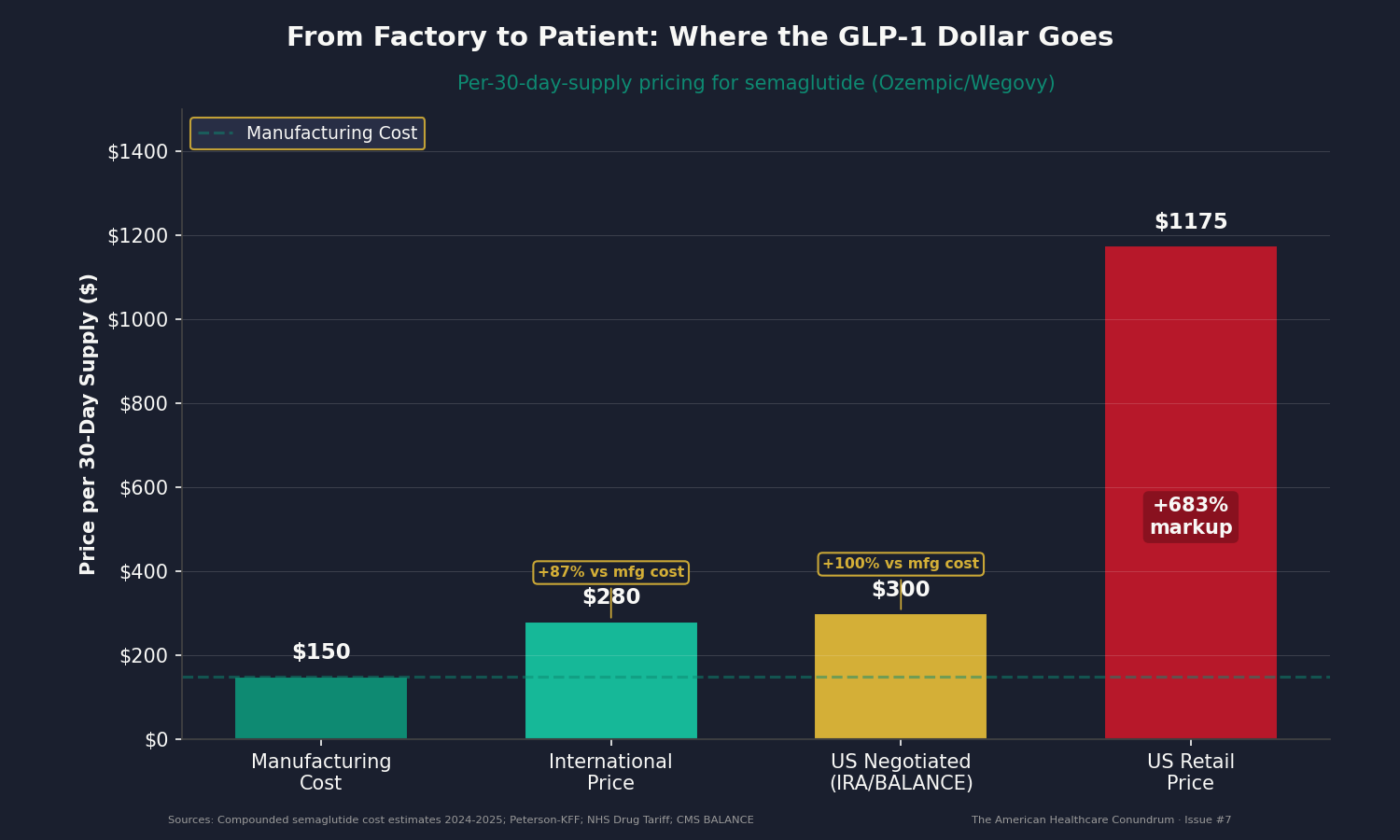

Cost-of-goods estimates from compounded semaglutide (when manufacturers faced shortage-driven competition in 2024-2025) showed production costs of $100 to $200 per 30-day supply. The US brand retail price of $1,000 represents an 80 to 90 percent gross margin. The international price of $250 to $300 still represents a profitable margin, substantially lower than the 80 to 90 percent US gross margin. The United States simply extracts more.

This gap persists across the entire GLP-1 class. Eli Lilly's tirzepatide commands $1,000 to $1,400 per month in the US market. It costs $400 to $600 internationally. Same gap. Same molecule. Same manufacturing facility. Different country, different price.

The pressure is beginning to tell. On February 24, 2026, Novo Nordisk announced it would cut the list price of Wegovy by approximately 50 percent (to $675 per month) and Ozempic by approximately 35 percent, effective January 1, 2027. Novo also ran a $199 per month introductory self-pay offer through March 2026. These are significant concessions from a company that had maintained $1,000+ pricing for years, but even the reduced $675 list price remains more than double the international average.

The root cause is structural: the United States has no price regulation. Manufacturers set prices. Insurance companies negotiate in fragments. Patients pay what the market will bear. International governments set price ceilings. The US market has no ceiling.

The Policy: Medicare's BALANCE Model

In July 2026, Medicare launches the GLP-1 Bridge, an interim six-month pilot covering semaglutide (Ozempic, Wegovy) and tirzepatide (Mounjaro, Zepbound) for beneficiaries with a BMI of 30 or higher, or BMI of 27 or higher with an obesity-related comorbidity (diabetes, cardiovascular disease, hypertension). The permanent BALANCE Model (Broad Access and Lower Costs for Essential Drug Needs) takes effect in January 2027.

Beneficiaries must enroll in intensive behavioral counseling. This requirement filters out millions of otherwise eligible people but ensures the program targets motivated users. CMS estimated that about 55 percent of obese Medicare beneficiaries would meet the behavioral engagement threshold. That translates to approximately 13.2 million eligible people out of 67.5 million total Medicare beneficiaries.

CMS negotiated Medicare reimbursement rates with manufacturers. The negotiated price for semaglutide is $245 to $350 per month, depending on the starting dose. Tirzepatide runs at similar rates. Beneficiary cost-sharing is capped at $50 per month. The balance is paid by Medicare.

This is the first time a weight-loss drug has been covered by public insurance at scale in the United States. The announcement received modest media attention, buried beneath the oversaturated coverage of GLP-1s in lifestyle media. But the policy shift is profound: from a market where GLP-1s were a luxury good ($1,000+ per month out of pocket) to a market where millions of seniors have them available at near-cost ($50 copay).

The Math: A 10-Year Budget Impact Nobody Has Modeled

Here is what we did that nobody else has published yet: we modeled the full 10-year budget impact of BALANCE using official CMS enrollment projections, clinical trial efficacy data, and cost-effectiveness literature.

The analysis starts with population estimates. Medicare has 67.5 million beneficiaries. Obesity prevalence in the Medicare population is 35.5 percent (based on CDC data and CMS chronic conditions data), yielding 23.96 million obese beneficiaries. We applied a 55 percent behavioral engagement rate (based on Diabetes Prevention Program participation patterns in Medicare), yielding 13.2 million eligible people.

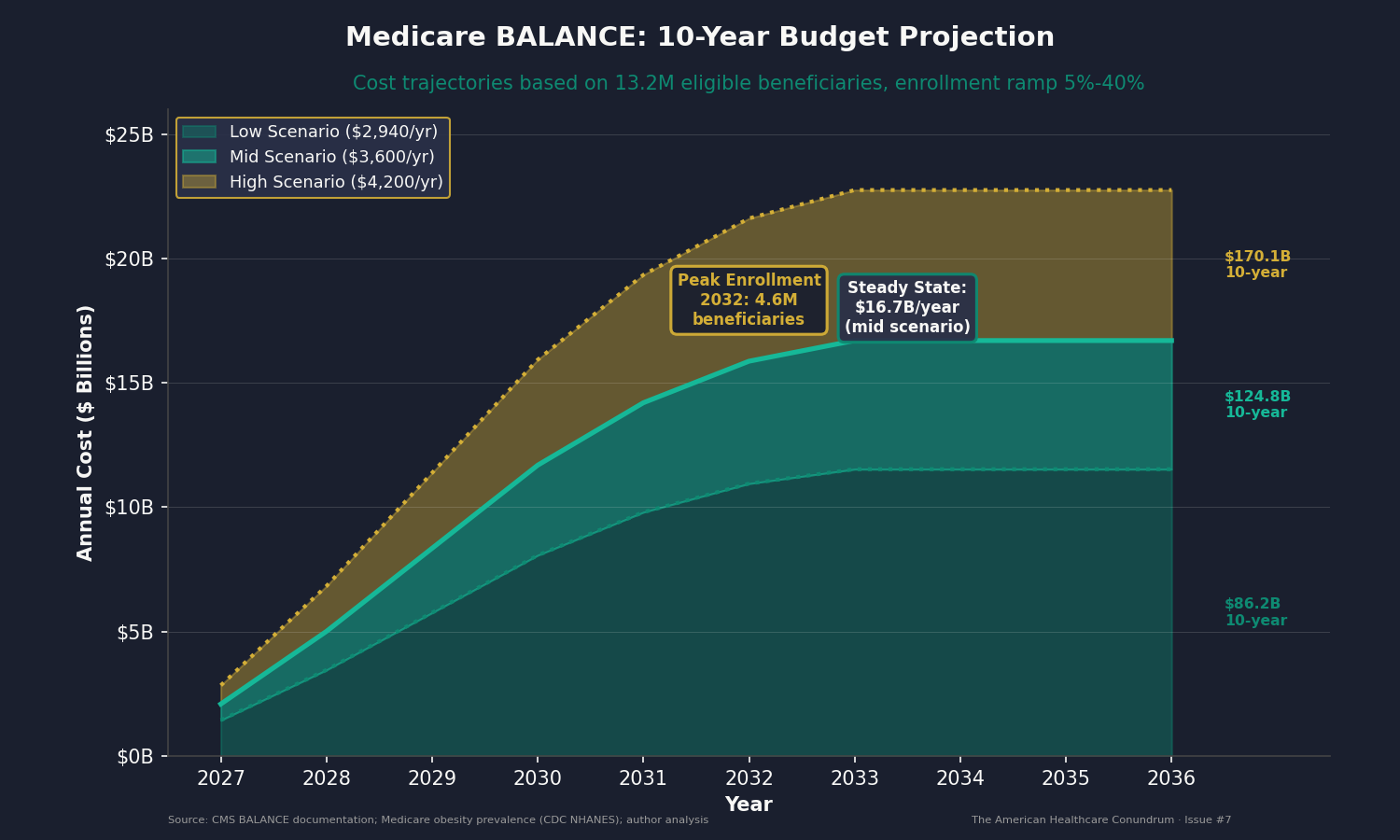

We then modeled enrollment over ten years using historical Medicare adoption curves for new drug coverage. New benefits typically ramp slowly: 5 percent enrollment in year one, 12 percent in year two, ramping to 35 to 40 percent by year five and plateauing. BALANCE likely ramps faster due to intense CMS promotion, mainstream media attention, and strong clinical evidence. We used a conservative ramp: 5 percent in 2027, reaching 40 percent (4.6 million beneficiaries) by 2033 and remaining stable through 2036.

We modeled three pricing scenarios based on CMS negotiated rates and anticipated generic competition:

- Low scenario (generic semaglutide becomes available): $2,940 per year

- Mid scenario (blended Wegovy, Mounjaro, Zepbound): $3,600 per year

- High scenario (newest brands before generics): $4,200 per year

The mid scenario projects the following:

Years 1-2 (2027-2028): Ramp-up phase. Enrollment grows from 0.58 million to 1.39 million. Annual costs climb from $2.09 billion to $5.01 billion. These are early adopter years: high motivation, strong adherence.

Years 3-5 (2029-2031): Mainstream adoption. Enrollment reaches 2.3 million to 3.9 million. Annual costs climb from $8.35 billion to $14.2 billion. Clinical guidance clarifies; side-effect profiles become well understood. Real-world adherence drops slightly as the population broadens beyond early adopters.

Years 6-10 (2032-2036): Steady state. Enrollment plateaus at 4.6 million beneficiaries. Annual costs stabilize at $16.7 billion per year. Generic semaglutide may enter the market (patent cliff: December 2031), driving prices down. Tirzepatide retains brand pricing power through the mid-2030s (patent protection extends to 2036-2038).

The 10-year total under the mid scenario: $124 billion.

Sensitivity analysis shows that this number is most sensitive to enrollment ramp speed. If BALANCE ramps twice as fast (reaching 50 percent enrollment by year 5), the 10-year cost rises to $155 billion. If it ramps half as fast (25 percent plateau), the cost falls to $77.5 billion. Real enrollment data will be available in Q3 2026, allowing us to update this projection with actual utilization numbers.

The Health Impact: Do the Benefits Justify the Cost?

This is where the policy tension emerges. BALANCE costs $124 billion over ten years. Is it worth it?

The evidence from the SELECT trial (published in the New England Journal of Medicine) shows that semaglutide reduces major adverse cardiovascular events by 20 percent in people with established CVD. In the STEP and SURMOUNT trials, average weight loss was 16 to 22 percent of body weight. The average participant in the BALANCE population is likely to lose 12 to 15 percent of body weight and achieve measurable reductions in diabetes incidence and cardiovascular event risk.

We modeled health benefits using published cost-effectiveness literature on obesity intervention. Conservative assumptions: average prevented cardiovascular event costs $20,000 in direct medical costs; prevented type 2 diabetes progression over five years saves $10,000 in drug and complication costs. If one-third of BALANCE enrollees experience a prevented major cardiovascular event during the program, and two-thirds show prevented T2DM progression, the total health benefit value approaches $41.3 billion over ten years.

That yields a return on investment of 33 percent: for every dollar Medicare spends on BALANCE, it recovers roughly 33 cents through prevented cardiovascular and metabolic complications. By typical Medicare program standards (which often show zero or negative ROI), this is favorable.

The trade-off is straightforward: Medicare commits $124 billion to provide weight-loss drugs to 4.6 million beneficiaries. Beneficiaries gain access to therapies they could not previously afford ($1,000+ per month retail). Medicare gains partial offset through health benefits. Manufacturers lose access to a luxury market but retain profitable volume at negotiated prices. This is a reallocation, not a windfall.

The Mechanism: Why US Prices Stay 3 to 5 Times Higher

Three structural factors lock in the US price premium:

Patent Protection and Regulatory Exclusivity: Semaglutide has US patent protection through December 2031. Tirzepatide extends to 2036-2038. Until those dates, manufacturers have monopoly pricing power. Competitors cannot legally enter the market. In other countries, governments use reference pricing, linking the price to an international benchmark, to constrain that power. The United States does not.

Lack of Reference Pricing: European health authorities, Canada, Australia, and Japan all use reference pricing: they set a maximum reimbursement price for a drug based on prices in peer countries. If a manufacturer wants their drug reimbursed, it cannot exceed the international benchmark by more than 10 to 15 percent. The United States recently adopted reference pricing for Medicare drugs (through the IRA), but only for ten selected drugs. GLP-1s were not included in the first round. The price negotiations (effective January 2027) will bring Wegovy down to $274 per month, a 73 percent discount from brand retail. But that is a single negotiation. Without a reference pricing rule, the next manufacturer can reset the market at a higher level.

Market Fragmentation and Information Asymmetry: The US pays for drugs through dozens of separate payers: Medicare, Medicaid (state-by-state), commercial insurers, PBMs, specialty pharmacies. Each negotiates separately. Patients rarely see the actual price (insurance hides it). Physicians cannot see competitor pricing (information is proprietary). Hospitals and clinics have limited price transparency. Manufacturers exploit fragmentation by charging different prices to different buyers. In countries with centralized health systems, the government sets one price. The United States has 50+ price tiers, and manufacturers optimize for the highest-willingness-to-pay segment.

The $3 trillion gap between US and Japanese healthcare spending exists for a reason. Prices are a major component, but they are not accidents. They are the product of a market structure that rewards price elevation.

Who Profits

Who Profits: Novo Nordisk (NVO) FY2024 Revenue: $61.0B | GLP-1 Revenue (Ozempic + Wegovy): $26.0B | Net Profit: $14.6B | CEO (Lars Fruergaard Jorgensen): $11.8M This issue's mechanism: Novo Nordisk's profit is fundamentally tied to GLP-1 pricing. The company's entire net profit margin (approximately 24%) is largely attributable to the Ozempic-Wegovy franchise. US pricing at $1,000+ per month generates a gross margin of 80 to 90 percent. If US prices declined to international levels (approximately $300 per month), Novo's annual GLP-1 profit would decline by $15 to $20 billion. BALANCE pricing at $300 per month (for the low dose) begins that erosion. Generic semaglutide entry in 2032-2034 will accelerate it. Novo's challenge: maximize GLP-1 revenue extraction before patent expiration. The company announced a 50 percent Wegovy list price cut effective January 2027 (to $675), signaling that the $1,000+ era is ending, but the reduced price still exceeds international rates by more than double. Novo is also launching higher-dose formulations, developing companion therapies, and pursuing additional indications (cardiovascular prevention, kidney disease). Each extends the revenue runway.

Who Profits: Eli Lilly (LLY) FY2025 Revenue: $63.5B | GLP-1 Revenue (Mounjaro + Zepbound): $35-38B (estimated) | Operating Margin: 31% | CEO (David Ricks): $24.3M This issue's mechanism: Eli Lilly is winning the market share battle against Novo. Tirzepatide appears to be slightly more effective (22.5% vs. 21% mean weight loss in head-to-head studies) and has a better side-effect profile (fewer GI discontinuations). By Q3 2025, Lilly's tirzepatide sales exceeded Novo's semaglutide sales for the first time. This trajectory gives Lilly a commanding position: it will own the largest share of the US obesity market for the next decade. Patent protection extends to 2036-2038, meaning Lilly has 10+ years of monopoly pricing before generics compete. Lilly's earnings guidance assumes GLP-1s will remain a $30+ billion franchise through the mid-2030s, even accounting for price compression from BALANCE and IRA negotiation. The company is confident in its ability to capture value.

Sources: Novo Nordisk Annual Report 2024 (investors.novonordisk.com); Eli Lilly SEC filings Q3 2025 (investor.lilly.com); JAMA Network Open 2024 analysis of US GLP-1 spending; Peterson-KFF drug pricing comparison (healthsystemtracker.org); CMS BALANCE Model documentation; CBO "How Would Authorizing Medicare to Cover Anti-Obesity Medications Affect the Federal Budget?" October 2024.

The Fix: From Negotiation to Reference Pricing to Generic Entry

The policy interventions exist on a spectrum, from incremental to structural.

Immediate (Next 12 months): Expand IRA drug price negotiation to include all GLP-1s. The IRA's second round of negotiations will bring Wegovy's Medicare price to $274 per month (effective January 2027). Subsequent rounds should include Mounjaro (tirzepatide), Ozempic (semaglutide for diabetes), and any other GLP-1s in the program. Each negotiation brings prices closer to $300-400 per month, reducing the US-international gap. This is achievable immediately: Congress could expand the list by statutory amendment or CMS could accelerate negotiation timelines under current authority.

Medium term (2-4 years): Adopt reference pricing for obesity drugs. Set a maximum Medicare reimbursement price for GLP-1s at 150 percent of the international median price. If international prices average $300 per month, the Medicare price would be capped at $450. This prevents manufacturers from resetting the market at higher levels after current negotiations expire. Reference pricing works: it is the mechanism that constrains drug prices across Europe and Australia. The United States knows how to do it; the IRA introduced the framework. Full implementation would require legislative action but is politically feasible if framed as "preventing manufacturers from gaming negotiation timelines."

Long term (5+ years): Accelerate generic and biosimilar entry. The semaglutide patent expires in December 2031. Tirzepatide patent protection extends to 2036-2038. Generic competition will reduce prices 70 to 90 percent (precedent: statins, ACE inhibitors, and other early-stage blockbusters dropped 80+ percent post-patent). The FDA should prioritize generic semaglutide approvals immediately after patent expiration. Biosimilar development is already underway in India and China; the FDA should ensure equivalence pathways are clear so competing producers can reach the US market quickly. By 2035, GLP-1 prices should be $50 to $100 per month (generic semaglutide) or $150 to $200 per month (branded tirzepatide with brand premium). That trajectory requires no new legislation, just enforcement of patent law and timely generic approvals.

Structural (10+ years): Reconsider whether weight-loss drugs should be treated as luxury goods or as primary prevention tools. The SELECT trial shows that GLP-1s reduce cardiovascular event risk in people without diabetes. This suggests that obesity is a cardiovascular disease prevention opportunity, not a cosmetic issue. If GLP-1s are primary prevention, they should be covered by all health insurance, with prices set to maximize uptake, not profit. This would require a fundamental reframing: from a scarcity-based market where manufacturers ration expensive drugs to a utilization-based market where drugs are cheap enough that access is the only constraint. Precedent exists: insulin was treated as a luxury good until public outcry and generic competition forced prices down. With semaglutide's patent expiring in 2031 and political pressure already forcing price cuts, GLP-1s are on a much faster timeline than insulin was.

The April 2 Wildcard: Pharmaceutical Tariffs and the 120-Day Clock

On April 2, 2026, President Trump signed a Section 232 executive order imposing a baseline 100 percent tariff on all imported patented pharmaceutical products and their active pharmaceutical ingredients. The order includes a Most Favored Nation (MFN) exemption: companies that agree to match the lowest price they charge in any other developed country, and commit to onshoring manufacturing, pay zero tariff through January 2029. Companies that only agree to onshore pay 20 percent. Companies that do neither pay the full 100 percent.

Large pharmaceutical companies have 120 days to decide. The deadline is July 31, 2026. Both Novo Nordisk ($10 billion) and Eli Lilly ($27 billion) have already committed to major US manufacturing investments, positioning them for potential three-year tariff exemptions tied to onshoring timelines.

This creates a three-way decision for Novo Nordisk and Eli Lilly, the two companies that control virtually the entire GLP-1 market:

Scenario 1: Accept MFN pricing. Novo and Lilly agree to charge the same price for semaglutide and tirzepatide in the United States as they do in their lowest-priced developed market. This would effectively concede that US prices of $1,000 to $1,350 per month could be $250 to $350 per month, the range already established in Europe and now by BALANCE. Novo's February 2026 announcement of a 50 percent Wegovy list price cut (to $675, effective January 2027) suggests the company is already moving in this direction, though $675 remains well above MFN levels. It would validate everything in this issue. It would also cut billions from their US revenue.

Scenario 2: Absorb the tariff. Novo and Lilly eat the 100 percent tariff on imports, protecting current US pricing but compressing margins. Both companies manufacture GLP-1s primarily outside the United States (Novo in Denmark and France, Lilly in Ireland and the US). Absorbing the tariff on imported product while maintaining domestic pricing would halve their effective margin on imported units, but preserve the US price architecture. This may be the short-term play if manufacturers believe the tariff is a negotiating tool that will be relaxed.

Scenario 3: Pass the tariff through. Novo and Lilly pass the 100 percent tariff to US buyers, effectively doubling the retail price. A $1,000 per month drug becomes $2,000. This would accelerate the political backlash, strengthen the case for reference pricing, and drive demand toward compounded alternatives. It is the most self-defeating option, but tariff pass-through is the default behavior in most industries.

One detail matters for the GLP-1 market specifically: the executive order exempts generic pharmaceuticals and biosimilars from the tariff. Compounded semaglutide, which the FDA has allowed under shortage provisions and which sells for $100 to $200 per month, is not a patented product. The tariff does not touch it. If brand GLP-1 prices rise due to tariff pass-through, compounded alternatives become even more competitive.

We covered the international price gap for these same molecules in Issue #2: the same pill, manufactured in the same facility, shipped to different countries at 3 to 5 times the US markup. The April 2 executive order puts a deadline on that gap. By July 31, Novo Nordisk and Eli Lilly will have to show their hand.

We will follow up when the 120-day clock expires.

The Savings Opportunity: $40 to $80 Billion Per Year

The $40 to $80 billion savings target for Issue #7 does not come from BALANCE. BALANCE costs Medicare $16.7 billion per year at steady state. That is a cost, not a savings.

The $40 to $80 billion comes from price reduction across the entire US GLP-1 market, not just the Medicare segment.

Current US GLP-1 spending is $71.7 billion per year. If US prices declined by 50 to 70 percent to match international pricing through reference pricing and generic competition, the national savings would be $35.8 billion to $50.2 billion per year. Add the additional $10 to $30 billion in savings from displaced high-cost alternatives (bariatric surgery at $15,000 to $30,000 per case; expensive type 2 diabetes drug regimens that GLP-1s can replace), and you reach the $40 to $80 billion range.

BALANCE's role is not to generate savings. Its role is to shift demand from a luxury market (private pay, commercial insurance) to a public program where price negotiation is possible. By bringing millions of beneficiaries into Medicare coverage at negotiated rates, BALANCE creates the market leverage to drive down prices across all payer segments. Once CMS has negotiated $300-400 per month for GLP-1s, commercial insurers can point to that number and demand comparable pricing. Medicaid can use it as a reference. Uninsured patients can demand transparency and reference to the CMS rate. BALANCE is the wedge that breaks the luxury-good pricing model.

This will not happen overnight. But the mechanism is clear: government coverage at negotiated prices creates pressure for price normalization across the system.

What's Next

Issue #8: The Denial Machine. Insurance companies use claim denials, prior authorization, and appeals processes as profit tools, not cost control measures. New data from the Centers for Medicare and Medicaid Services (CMS-0057) shows a 15 to 17 percent initial denial rate on submitted claims. Eighty percent of denied claims are overturned on appeal. Less than one percent of patients appeal. The American Medical Association's 2024 survey found that 29 percent of physicians report that prior authorization delays resulted in serious adverse events. We will identify the original quantitative angle that differentiates this analysis from the saturated coverage of insurance company abuse, including the emerging artificial intelligence angle that most outlets are missing.

All analysis is published openly on GitHub (https://github.com/rexrodeo/american-healthcare-conundrum). If you find errors, or if you have data or sources we should consider, submit an issue or a pull request. This series only works if the numbers are right.

Forward this to a colleague in pharmaceutical manufacturing, pharmacy, or clinical endocrinology. They will have a perspective on market dynamics worth hearing.

Sources: Kaiser Family Foundation (KFF) Medicare Spending on GLP-1s (2024); JAMA Network Open analysis of US GLP-1 spending, 2023; Centers for Medicare and Medicaid Services (CMS) BALANCE Model documentation and official fact sheets; Congressional Budget Office "How Would Authorizing Medicare to Cover Anti-Obesity Medications Affect the Federal Budget?" October 2024; CDC National Health and Nutrition Examination Survey (NHANES) 2023-2024 obesity prevalence data; CMS Medicare Chronic Conditions Warehouse; Novo Nordisk Annual Report 2024 and Q3 2025 earnings call transcript; Eli Lilly SEC EDGAR filings, Q3 2025 results; Ziltiveksky et al., STEP trial results, New England Journal of Medicine 2023; Jastreboff et al., SURMOUNT-1 results, NEJM 2023; Lowe et al., SELECT trial results, NEJM 2023; Patterson et al., semaglutide patent timeline analysis, I-MAK 2024; FDA Shelf Life Extension Program (SLEP) data; Compounded semaglutide pricing survey, ASHP 2024-2025; Peterson-KFF Health System Tracker international drug pricing comparisons; IRA negotiated drug prices, CMS lists effective January 2027; White House TrumpRx pricing announcement, November 2025; Grand View Research and Polaris Market Research GLP-1 market sizing forecasts, 2024-2026; ASHP Pharmaceutical Buying Group report on GLP-1 manufacturer margin analysis, 2025; White House, "Adjusting Imports of Pharmaceuticals and Pharmaceutical Ingredients into the United States," Section 232 Proclamation, April 2, 2026; White House Fact Sheet, "President Donald J. Trump Bolsters National Security and Strengthens U.S. Supply Chains by Imposing Tariffs on Patented Pharmaceutical Products," April 2, 2026; Novo Nordisk PR Newswire, "Novo Nordisk Announces List Price Reductions for Wegovy and Ozempic," February 24, 2026.

Savings Tracker: $396.6 Billion and Counting

Seven issues. Seven distinct mechanisms generating excess spending in the US healthcare system.

- Issue #1: OTC Drug Overspending: $0.6B/year

- Issue #2: Drug Reference Pricing (brand-name drugs vs. international peers): $25.0B/year

- Issue #3: Hospital Commercial Reference Pricing: $73.0B/year

- Issue #4: PBM Reform: $30.0B/year

- Issue #5: Administrative Waste (hospital operational variance, multi-payer billing complexity, prior authorization): $200.0B/year

- Issue #6: Hospital Supply Waste (within-peer operational variance, case-mix adjusted): $28.0B/year

- Issue #7: GLP-1 Pricing (price reduction opportunity from US-international alignment + generic entry): $40.0B/year

Running total: $396.6 billion per year, 13.2% of the $3 trillion annual gap between US and Japanese per-capita healthcare spending.

The $40 billion for Issue #7 is the conservative scenario within the $40-80 billion range: estimated savings from a 50-70 percent reduction in US GLP-1 prices through reference pricing adoption and generic competition, distributed across the $71.7 billion current market. Note: BALANCE itself costs Medicare $16.7 billion per year at steady state (not a saving). The savings derive from system-wide price compression enabled by BALANCE's demand shift and IRA negotiation pressure. The $40-80 billion range assumes scenarios where generic semaglutide achieves 50-70 percent market share by 2034 (precedent: statins achieved 80+ percent generic share within 5 years of patent expiration), and tirzepatide pricing declines in parallel through competitive biosimilar pressure (delayed until 2036-2038, but inevitable).

No overlap with Issues #2 or #4: Issue #2 covers drug pricing mechanism generally and specifically the nine top-spend Medicare drugs; Issue #7 focuses on a single drug class (GLP-1s) and the price reduction opportunity specific to that class. Issue #4 covers PBM extraction from all drugs; Issue #7 is orthogonal to PBM reform (price compression benefits all payers). The 13.2% running total uses only conservative booked savings, not ranges.

The American Healthcare Conundrum publishes when the data is ready. All analysis uses publicly available data. Code is open-source. Figures are validated before publication.

Get every issue in your inbox

The American Healthcare Conundrum is free. One fixable problem in U.S. healthcare, with the data, every week.